The Ground We Stand On

03/17/25 The Monday Blueprint:

TL:DR: In "The Debt Lie," the first in a three-part series, I break down how Dave Ramsey and Suze Orman’s no-debt gospel kept me broke, and why avoiding debt isn’t the answer—learning to use it is. The essay reviews are meditations on failure and obsession, beauty as power and hunger, and our craving for disruption with real-world disaster. Meanwhile, the market report reveals a financial system bracing for impact—tariffs, inflation, and uncertainty are shaking the ground beneath us.

The Debt Lie: What They Never Told You About Money

This is Part One of a three-part series, The Debt Lie: What They Never Told You About Money. For years, I believed what financial gurus like Dave Ramsey and Suze Orman preached—that debt was the enemy, and that financial freedom meant cutting back, living small, and staying out of the red. But after watching my dad go bankrupt, struggling through my own financial disasters, and realizing that playing by their rules left me broke, I started to see the truth: avoiding debt wasn’t the key to success—learning how to use it was. In Part Two, I’ll explore the only two real ways to improve your finances: spend less or make more. And in Part Three, I’ll break down why debt isn’t just okay—it’s often necessary.

In 1998, we all married—me, my brother, and my sister. Also, my dad filed for Chapter 7 bankruptcy.

He sucked down little brown cigarillo and I put away Camel Blues way faster than I should have. The bank was getting ready to take the house. He crushed out the cigarillo into the Maxwell House can we used for an ashtray. He said had nothing to give me for the wedding, and that he was scared because he had no idea what he was going to do the next day. That was the most vulnerable my father has ever been with me. He’d built a lumber brokerage, took out loans to keep it running, and when the business couldn’t stay afloat, the bank came calling. The debt was around $185,000—a number that seemed impossible at the time, a financial ruin so severe it forced a complete reset.

Twenty-six years later, I look at my financial situation and laugh because, between my wife and I, we owe nearly double that in student loans. And unlike my dad’s bankruptcy, which had a clear ending, this debt isn’t going anywhere. It lingers and reshapes how I think about money, ownership, and the kind of future I want to build.

Once Mary and I moved into a big, empty duplex on Clinton Street in Columbus, Ohio—so empty we didn’t even have enough furniture to fill it—I painted apples along the tops of the kitchen walls. That’s when Mary started watching The Suze Orman Show, while I just sat back and watched how ruthless Orman was to every caller. How mean she could be. How insulting and condescending.

At the same time, while driving around late at night delivering Domino’s, I listened religiously to Dave Ramsey. I’d hear callers “ring the bell” and shout, We’re debt-free! like they had just won their freedom. Ramsey, at least, seemed more celebratory.

Mary and I did not have our college degrees at this point. We had some credit card debt that seemed impossible to get out from underneath. We had a Chevrolet Cavalier we owed money on that kept breaking down, and we seemed to have to make the choice each month whether we were going to make the car payment or make the repair. I think, to this day, that car may have been haunted. Orman and Ramsey’s debt-free living advice seemed not only right but morally right. And I felt pretty damn scared we’d never recover financially from the debt.

By 1986, Ramsey had built a real estate portfolio worth over $4 million, financed heavily through loans. The aggressive leveraging caught up to him, and in 1988, he filed for bankruptcy. That’s when he pivoted to financial counseling. But while Ramsey preached running a business without debt—no loans, no credit cards, no lines of credit—by 1996, he was right back at it, securing a loan to finance more real estate.

Maybe that’s why my wife liked Orman more than Ramsey—at least Orman practiced what she preached. But either way, both financial gurus weren’t selling freedom. They were selling fear—packaged neatly for the upper lower and middle class.

During the 2008 financial crisis, I decided it was time to start a business. I secured two loans—one from my wife’s parents, and the other from her brother. But for the most part, I followed Ramsey’s no-debt rule. We paid cash for equipment, locked in space in a hotel kitchen, and had everything ready to go. Seating for 125. A bar for another 75. Catering contracts signed. Food prepped. And a kick-butt pizza shop named “Sauced.” We were set.

And then, two weeks before opening, the hotel owner called me.

“Hey, yeah, just so you know, I’m not paying my mortgage anymore, and the bank is kicking you out.”

That was it. The whole thing—$40,000 in family loans and personal savings—vanished overnight. There was no backup plan, no slow unraveling, just a hard stop.

A little carryout shop had just become available down the road—small, manageable, a real chance to salvage something. But we had spent every last dollar. No debt. No leverage. No way to pivot. I had done everything “the right way,” just like Ramsey preached. And it left me with nothing.

The next few years were a string of unreliable jobs—midnight shift gas stations, more pizza delivery. Anything to keep the lights on. Some nights, dinner came from the Cargill warehouse where my dad worked, the expired food he brought home just one more reminder of how close we were to the edge. I remember distinctly one October buying a pumpkin to carve out a Jack-o-Lantern for my daughter—but we stretched that single pumpkin for days. Stew, cake, roasted snacking seeds. Looking back, I have no idea how many meals we got out of it, but I was pretty proud of my resourcefulness.

The pumpkin meals happened at the same time I applied for food stamps. I didn’t know it then, but my sister-in-law was the one doing exit interviews for SNAP applicants. One of her jobs was handing out nutritional recipes to people in my exact situation, and when my turn came, she slid a card across the table for an easy pumpkin strudel. It was at that moment I decided I’d go back to school, get my graduate degree, and teach. My wife asked me how we were going to afford such an endeavor. I mean, our bank accounts were totally zapped. And I said, going against everything Suzie Orman had been preaching to my wife, against everything Dave Ramsey had been cramming down my throat, much like that pumpkin strudel, I said, “Federal Student Aid Loans.”

The idea here was that once I had that degree, I’d be able to secure the W-2 job that would allow me to not be broke anymore. And the debt, I’d be able to escape. Except, I kept running into professors in grad school who told me that I shouldn’t think about student loans as anything I should pay back, but more like ongoing dues that allowed me to belong to a very specific country club.

The idea was simple: get the degree, secure the W-2 job, and escape being broke. And the debt? I’d pay it off.

Except, by the time I graduated in my late 30s and racked up all that debt, academia had changed. Full-time jobs were near impossible to find, and after nine years as a W-2 adjunct, I saw exactly how the system worked.

The union-controlled pay slots locked us all in. Seniority, not skill, dictated raises. The longer you stuck around, the more you made—but only up to a hard cap. If CCSNH never hired another adjunct, eventually, we’d all be making the same amount. It didn’t matter that I had better student outcomes, higher engagement, or that I was more invested in the work. No matter my productivity level, I wasn’t going to get paid more.

And it wasn’t just academia.

Straight out of high school, I worked at Hoge Lumber Company—the same company my grandfather worked at, the same one my dad and brother worked at. A generational tradition. Then they brought in a single computerized saw, and that machine glitched out for five, six hours at a time. I told my dad I was sick of stacking lumber at the end of the line when I knew I could run that machine better than anyone.

I didn’t expect him to say anything, but one day, at a coffee shop, he ran into the CEO and told him about my complaint. Next thing I knew, I was running the machine. I processed lumber through so fast, we ran out of wood. My productivity was worth literally ten people on hand saws.

My pay never went up a dime.

And then the floor manager shut me down.

“If we let that machine run like that, all these people are going to lose their jobs.”

Orman, Ramsey, my dad all preached the same refrain though: work hard so you can make more money at your W-2, and live small and debt-free. I couldn’t just keep stacking lumber at someone else’s saw. And after nine years of adjuncting, and starting to slip into my fifties, I couldn’t keep waiting for the Community College System of New Hampshire to decide I was worth more. Somehow, I felt the game was rigged. And I needed a different way to play. I needed to stop focusing on how little I could spend and start figuring out how much more I could make. This last year that I taught in 2024 I made just under $18,000 from my CCSNH W-2. And from this past November to February, I grossed approximately $28,000 in real estate. And to get started in real estate, I had done exactly what I had done with my education. I took out loans. Only this time, instead of federal funding, they were high-interest credit cards.

IN NO PARTICULAR ORDER

Essays I’ve Read

Wattle by Mark Gozonsky is a weird little essay that doesn’t immediately declare upfront its theme. You are dropped right into Abner’s interest in cloning an apple tree—and we don’t even know who Abner is, or why Abner is important, much less do we even understand why he wants to clone an apple tree. And I’m not clear until a third of the way through where Wattle is taking us. The overall structure feels loose. That’s maybe the best way to describe Gozonsky’s tone and voice.

Part of the charm of Wattle is how Gozonsky embraces tangents.

Abner is both an earnest craftsman and an absurd figure, hacking at trees with a foldable hacksaw, sweating through his calamine-streaked shirt. His DIY determination borders on the obsessive, yet the essay isn’t in a hurry to get to a point. Gozonsky moves from apple trees to deer fencing to etymology. The reader is never sure what’s around the next bend.

In the end, Abner’s apple grafts fail, but something still grows, and that feels like Wattle’s ultimate lesson. Success isn’t always what you planned, but the act of doing, of trying, still leaves something behind. A fence, a tree. Maybe a story.

In French, essai does indeed mean essay as in academic or literary, but also means attempt or trial, as in trying something out, and essai is famously linked to Michel de Montaigne, whose Essais (1580) established the modern form of the personal, reflective essay. I think that the second definition of essay, that exploration of ideas, an experiment in thought, well, Wattle is the epitome of.

This is visceral, hypnotic, and sharp-edged in its hunger. Sherry Ning’s I Want to be Beautiful thrums with a kind of intoxicating longing—not just for beauty, but for power, for permanence, for transcendence. There’s something both ancient and ultra-modern in the way it frames beauty as both a curse and a weapon, a prayer and a possession. It’s Sylvia Plath in a mirror-lined dressing room, Anaïs Nin scrawling secrets in the margins, Botticelli’s Venus with blood under her nails.

Some standout lines that made me pause and feel something:

“I'm not just moisturizing, I'm conducting a seance to resurrect my glow.” That’s the kind of line that lingers, half-camp, half-sacrament.

“I want to be impossible to photograph correctly, never quite real except in person, where I devastate.” There’s so much myth-making here—beauty as a mirage, something you can’t quite pin down.

“I want to be a Klimt, skin pressed with gold leaf like a Byzantine icon, passion made holy.” Yes. Yes. Yes. This is beauty not as mere aesthetics, but as legend.1

But beneath the sultry, dazzling opulence, there’s a quiet whispered ache. And my real estate coach asked me what my big why was the other day, and I said that I wanted to be famous after I was dead.

My wife purchased a living off-the-grid survival guidebook that I think maybe she's opened once or twice to peruse. I keep thinking we need a small solar panel out our bedroom window to collect the sun's energy during the day to plug my CPAP into in case the power ever goes out. And I remember listening to Art Bell's Coast to Coast AM talk radio advertising hand-cranked radio/flashlight combos. My friend Mira Ptacin has written about doomsday bunkers and prepper moms. Lately, I’ve been thinking about my own shifting landscapes—both literal and metaphorical. My work, my writing, and my influence are all evolving. Even my physical space is changing: with my oldest kid moving out, I’m taking over her bedroom as my office. And then there’s the way I walk now, adjusting to a fused ankle—the quicksand beneath me no longer hollow but finally solid. I think about death more than I probably should, that if I’m lucky, I have maybe another good thirty years left. And that’s about it.

Jonah Walters’ Rip in the World is a gripping, beautifully woven piece that blends the personal, the scientific, the philosophical, and the literary. He explores the connection between volcanic eruptions and our subconscious craving for disruption, all while preparing for his move to LA, where earthquakes became his looming fear. His mother tells him to buy a heavy table. This was written in October 2024, and I can’t help but wonder how he fared during the January 2025 LA fires—if he knew, on some level, that his essay about fire was a kind of foreboding.

Maybe we read and write about fire, about disaster, about the shifting ground beneath us, only later to realize we were preparing for something unforeseeable.

Or maybe because we’ve lived through years of global instability—mass death, political chaos, existential threats stacking on top of each other—that we are intrinsically drawn to images of the earth cracking open, of cities burning, of lava pouring over landscapes. Maybe watching disaster unfold in real-time is a way of externalizing the chaos we’ve already been carrying. Or maybe a twisted kind of catharsis, a reminder that destruction has always been part of the human experience, that it’s not just this moment that feels apocalyptic.

Walters hints at why we’re drawn to this destruction—our craving for disruption, our need to be tested, the sense of powerlessness that disaster removes from us by making us mere observers—but he doesn’t land on any definitive answer. Maybe because there isn’t one. Or maybe because the real answer is too big, too tangled in history, psychology, and trauma.

LAST WEEK IN THE STOCK MARKET:

I Picked the Wrong Week to Quit Sniffing Glue: Tariffs, Inflation, and the Fed Keep Investors on Edge

The stock market ended the week in turbulent waters as investors wrestled with rising tariffs, inflation concerns, and an uncertain Federal Reserve outlook. A brief Friday rebound provided some relief, but major indices remain in correction territory, signaling persistent unease.

The S&P 500 edged up 0.57%, the Dow Jones gained 0.48%, and the Nasdaq climbed 0.62%, though all three remain well below recent highs. Bitcoin tumbled 11.61% as risk-off sentiment dominated, while Philip Morris surged 26.2%, reflecting a shift toward defensive plays amid economic uncertainty.

Bond markets stayed relatively steady, with the 10-year Treasury yield at 4.30%, as investors weighed the Fed’s next move. Commodities saw mixed action—Crude oil rose 1.00% to $67.85 per barrel, while gold ticked up 0.11% to $3,004.50, reflecting choppy risk sentiment.

With the Fed’s rate decision, upcoming earnings, and geopolitical tensions looming, markets are likely to remain volatile in the weeks ahead.

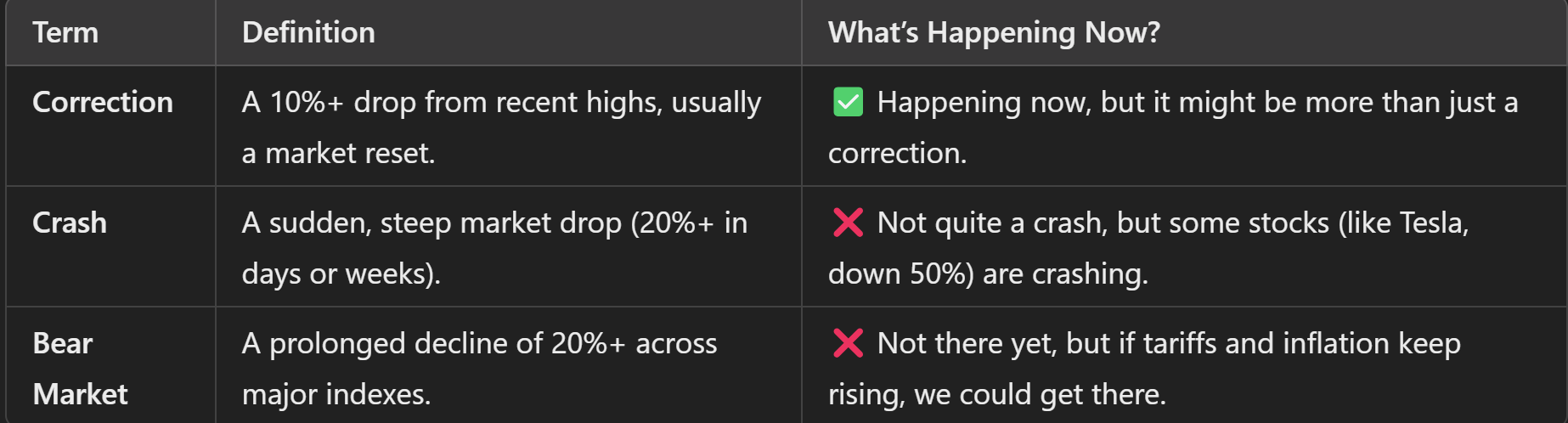

They call it a "correction" because the idea is that the market was overvalued or too high, and now it's "correcting" itself to a more reasonable level.

But here’s the problem: Not all drops are true corrections. Sometimes, the market isn’t just cooling off—it’s reacting to real economic problems.

This doesn’t look like a normal correction caused by market overexuberance. Instead, this drop seems driven by real economic fears tied to:

Trump’s tariffs raising costs for businesses and consumers.

Inflation expectations surging (highest since 1991).

Investors pulling out of riskier assets like Bitcoin and tech stocks.

Stagnating economic growth making people worried about recession.

Calling it a “correction” makes it sound normal, but what about all those smokers?

Philip Morris is up 26.2% while the rest of the market is down. This lines up with past market corrections.

2008 Financial Crisis: Cigarette sales barely dropped, even as consumers cut spending elsewhere.

COVID-19 Pandemic: Tobacco stocks outperformed the market as people turned to smoking and drinking more.

So yeah, people are smoking through the pain.

Big Themes to Watch:

1. The Fed’s Next Move: Rates on Hold, but for How Long?

The Federal Reserve is widely expected to keep interest rates steady at its upcoming meeting, but the real question is when (or if) rate cuts will happen this year. Markets had priced in three cuts, but rising inflation expectations and tariff-driven price hikes could push the Fed to stay cautious. Powell’s press conference and the updated “dot plot” will be key signals for how the central bank is thinking about inflation, growth, and future monetary policy.

2. Tariffs and the Ripple Effect on Supply Chains

The latest wave of tariffs on imported goods, from steel and aluminum to consumer electronics and appliances, is already driving up costs for businesses. Homebuilders are warning that tariffs on lumber and construction materials could add $7,500–$10,000 to the price of a new home, further squeezing an already fragile housing market. Meanwhile, companies with high international exposure (think Nike, FedEx, and tech manufacturers) are preparing to report earnings with a watchful eye on how tariffs are impacting costs and demand.

3. Stagflation Risks: Slowing Growth Meets Sticky Prices

The economy is sending mixed signals—job growth remains solid, but consumer sentiment is sinking, and inflation expectations are rising. The worst-case scenario? Stagflation, where economic growth stalls while inflation persists. If tariffs continue to push prices higher while business activity slows, the Fed may find itself trapped between keeping rates high to fight inflation and cutting rates to avoid recession.

4. Defensive Plays Take the Lead

With markets in correction territory, investors are shifting toward defensive stocks, including consumer staples, healthcare, and dividend-paying companies. The recent surge in Philip Morris (+26.2%) is a prime example of investors piling into “sin stocks”—businesses that tend to perform well when economic uncertainty spikes. Expect utility stocks, food & beverage companies, and healthcare giants to attract more attention in the weeks ahead as investors look for stability in a volatile environment.

Looking Ahead:

1. Market Volatility Isn’t Going Anywhere

With the Fed’s decision looming, earnings season kicking off, and tariffs creating supply chain headaches, expect continued swings in the market. Investors will be closely watching corporate earnings reports to gauge how businesses are handling rising costs and slowing demand.

2. The Housing Market Faces More Pressure

Rising construction costs from tariffs on lumber, steel, and appliances are making homebuilding more expensive, just as high mortgage rates continue to weigh on buyers. The next batch of housing data (home sales, permits, and starts) will reveal if demand is holding up or if buyers are finally hitting their breaking point.

3. Will the Fed Blink on Rate Cuts?

The Fed has signaled a "wait and see" approach, but if economic data starts turning negative—especially on jobs, retail sales, or corporate earnings—pressure to cut rates sooner could build. Markets currently expect the first rate cut by summer or fall, but sticky inflation and trade uncertainty could delay that timeline. Powell’s press conference will be crucial in shaping those expectations.

4. The Return of Recession Talk?

So far, the economy has avoided a hard landing, but warning signs are flashing. Long-term inflation expectations just hit their highest level since 1991, consumer sentiment is dropping fast, and tariffs are adding new uncertainty. If economic data weakens, expect renewed fears of a recession—and a market that reacts accordingly.

I have that poster in my house.